On Exponent, the weekly podcast I host with James Allworth, we discuss A Regulatory Framework for the Internet.

Listen to it here.

On the business, strategy, and impact of technology.

On Exponent, the weekly podcast I host with James Allworth, we discuss A Regulatory Framework for the Internet.

Listen to it here.

This week, when the U.K.’s Secretary of State for Digital, Culture, Media and Sport and the Secretary of State for the Home Department released a white paper calling for significantly increased regulation for tech companies, the scope of the debate was predictable. The MIT Technology Review laid it out succinctly:

Technology giants will be forced to have a “duty of care” for their users, if a proposal announced by the government on Monday becomes law. The proposal — a “white paper,” in UK legal parlance, which is one of the first stages of a formal government policy — is, on the surface at least, sweeping in scope and is a serious shot across the bows for big tech companies. But it has also raised some serious concerns about how it will be implemented and the possible consequences it might have on citizens’ free speech…

The proposals have raised interest among academics and observers, and alarm among privacy campaigners. The former note that while the document is scant on details despite being tens of thousands of words long, it sets out a clear direction in a way few countries have been willing to do. But the latter fear that the way it is implemented could easily lead to censorship for users of social networks rather than curbing the excesses of the networks themselves.

This proposal comes on the tail of an exposé in Bloomberg entitled YouTube Executives Ignored Warnings, Letting Toxic Videos Run Rampant; the debate around that piece, which I wrote about last week in two Daily Updates (here and here), not only touched on the question of free speech, but also the sheer scale of the problem — and, relatedly, the sheer scale of Facebook of Google.

In short, there are clear questions that arise around all of these exposés and proposals:

You can see how these questions quickly arrive at competing answers when looking at recent attempts at regulation:

At the same times, the Christchurch video and its spread are clearly problematic — there is something off about the current state of affairs.

It hardly bears noting that in a pre-Internet world there would be no widespread video of the Christchurch hate crime. Capturing video required specialized equipment, and more importantly, broadcasting video was limited to a small number of television stations, all of which, even if they had the video, would have exercised their editorial judgment to keep it off the air.

What is critical to note, though, is that it is not a direct leap from “pre-Internet” to the Internet as we experience it today. The terrorist in Christchurch didn’t set up a server to livestream video from his phone; rather, he used Facebook’s built-in functionality. And, when it came to the video’s spread, the culprit was not email or message boards, but social media generally. To put it another way, to have spread that video on the Internet would be possible but difficult; to spread it on social media was trivial.

The core issue is business models: to set up a live video streaming server is somewhat challenging, particularly if you are not technically inclined, and it costs money. More expensive still are the bandwidth costs of actually reaching a significant number of people. Large social media sites like Facebook or YouTube, though, are happy to bear those costs in service of a larger goal: building their advertising businesses.

The key differentiator of Super-Aggregators is that they have three-sided markets: users, content providers (which may include users!), and advertisers. Both content providers and advertisers want the user’s attention, and the latter are willing to pay for it. This leads to a beautiful business model from the perspective of a Super-Aggregator:

Everything is aligned from the Super-Aggregator perspective: users give attention that content providers work to earn, and advertisers compete to buy their way in.

Moreover, this arrangement allows Super-Aggregators to be relatively unconcerned with what exactly flows across their network: advertisers simply want eyeballs, and the revenue from serving them pays for the infrastructure to not only accommodate users but also give content suppliers the tools to provide whatever sort of content those users may want.

That, there, is the rub: given that these platforms are basically reflections of humanity, what users want varies from the beautiful to the profane — and things far more ugly than that. And worse, there is no editorial judgment to keep users from what they want, or suppliers from providing it. Indeed, that such sordid content can exist on YouTube and Facebook is testament to just how popular they are; that such content is effectively incentivized speaks to the fact that YouTube and Facebook’s moneymaking mechanism is completely divorced from this content match-making.

This is, in its own way, a market failure, albeit not, to be clear, in an economic sense: the allocation of goods and services by a Super-Aggregator is not only efficient, but also generates significant consumer surpluses. The failure, rather, comes from videos like that of the Christchurch massacre, or problematic YouTube content. It is not good for society that terrorists be able to freely broadcast their videos, or that child-exploitation videos spread on YouTube.

The problem is that there is no way to check this behavior: the vast majority of Facebook and YouTube users self-select away from this content, and while advertisers raise a fuss if they find out their ads are alongside this content, they have no incentive to leave the platforms entirely. That leaves Facebook and YouTube themselves, but while they would surely like to avoid PR black eyes, what they like even more is the limitless supply of attention and content that comes from making it easier for anyone anywhere to upload and view content of any type.

Note how much different this is than a traditional customer-supplier relationship, even one mediated by a market-maker: users disgusted by Uber, for example, could switch to Lyft, directly impacting Uber’s bottom-line. Or go back a few years, when GoDaddy expressed support for SOPA copyright legislation: the company was forced to change its position in the face of widespread boycotts (including by yours truly). When users pay they have power; when users and those who pay are distinct, as is the case with these advertising-supported Super-Aggregators, the power of persuasion — that is, the power of the market — is absent.

There are, in Internet parlance, three types of “free”:

Most in the West agree, at least in theory, with the idea that the Internet should preserve “free as in speech”; China in particular represents a cautionary tale as to how technology can be leveraged in the opposite direction. The question that should be asked, though, is if preserving “free as in speech” should also mean preserving “free as in beer.”

Specifically, Facebook and YouTube offer “free as in speech” in conjunction with “free as in beer”: content can be created and proliferated without any responsibility, including cost. Might it be better if content that society deemed problematic were still “free as in speech”, but also “free as in puppy” — that is, with costs to the supplier that aligned with the costs to society?

This distinction might square some of the circles I presented at the beginning: how might society regulate content without infringing on rights or destroying competitive threats to the largest incumbents?

Start with this precept: the Internet ought to be available to anyone without any restriction. This means banning content blocking or throttling at the ISP level with regulation designed for the Internet. It also means that platform providers generally speaking should continue to not be liable for content posted on their services (platform providers include everything from AWS to Azure to shared hosts, and everything in-between); these platform providers can, though, choose to not host content suppliers they do not want to, whether because of their own corporate values or because they fear boycott from other customers.

I think, though, that platform providers that primarily monetize through advertising should be in their own category: as I noted above, because these platform providers separate monetization from content supply and consumption, there is no price or payment mechanism to incentivize them to be concerned with problematic content; in fact, the incentives of an advertising business drive them to focus on engagement, i.e. giving users what they want, no matter how noxious.

This distinct categorization is critical to developing regulation that actually addresses problems without adverse side effects. Australia, for example, has no need to be concerned about shared hosting sites, but rather Facebook and YouTube; similarly, Europe wants to rein in tech giants without — and I will give the E.U. the benefit of the doubt here — burdening small online businesses with massive amounts of red tape. And, from a theoretical perspective, the appropriate place for regulation is where there is market failure; constraining the application to that failure is what is so difficult.

The result is a regulatory framework that looks like this:

“Free as in speech” is guaranteed at the infrastructure level, the market polices platform providers generally (i.e. “free as in puppy”), while regulation is narrowly limited to businesses that are primarily monetized through advertising (i.e. “free as in beer”) and thus impervious to traditional content marketplace pressures.

This framework, to be clear, leaves many unanswered questions: what regulations, for example, are appropriate for companies like YouTube and Facebook? Are they even constitutional in the United States? Should we be concerned about the lack of competition in these regulated categories, or encouraged that there will now be a significant incentive to build competitive services that do not rely on advertising? What about VC-funded companies that have not yet specified their business models?

Still, I think this framework provides a very important foundation for addressing many of the flaws in today’s regulatory proposals, particularly the unintended effects on small-and-medium sized businesses and the platforms that support them which, I believe, are critical for the economy of the future. Regulators and lawmakers should, as always, be wary that in the well-meaning attempt to shape the world as it is they foreclose the world that might be.

On Exponent, the weekly podcast I host with James Allworth, we discuss the question of YouTube, why it’s similar and different from Facebook, and why engagement is both alluring and a potential problem.

Listen to it here.

Tim Cook closed yesterday’s Apple event with these words:

From everything we’ve shared with you, you can see how important these services are for us and for all the ways they extend the experiences of our customers even further. They entertain, inspire, inform, and enrich our lives. Because at Apple, the customer is, and always will be, at the center of everything that we do.

It’s a short statement, but a useful way to think about the event specifically, and the state of Apple generally.

Frankly, not much; there were far more announcements that were coming in the summer or fall than were ready today or in the next couple of weeks:

Just as disconcerting was the lack of pricing information: Apple News+ is $9.99, and the Apple Card has no fees…and that’s all we know.

This raises the question of what the point of having this presentation now was. In an interview on the Accidental Tech Podcast about Apple’s upcoming Worldwide Developers Conference (WWDC) Senior Vice President of Worldwide Marketing Phil Schiller said:

We think about the audience for the keynote at WWDC as really three unique audiences. And the opening keynote is different than the rest of the week’s events and activities. That opening audience is developers, it’s customers, and of course it’s the press. Three unique audiences…

Of course this event was considerably different than WWDC, and so was the intended audience. Developers for the most part are out (although Apple Arcade is of interest), and while these services are certainly meant to be consumed by customers, the fact that most won’t launch for a while dulls the benefits Apple will gain from press coverage.

That leaves an unmentioned fourth audience: Wall Street. To that end, perhaps the more relevant comment from an Apple executive came in Tim Cook’s January Letter to Investors revising Apple’s guidance for 1Q2019:

We can’t change macroeconomic conditions, but we are undertaking and accelerating other initiatives to improve our results.

At the time Cook only mentioned improving the iPhone trade-in process, but it certainly seems possible that announcing so many new services so far ahead of their launch was an attempt to deliver on that promise ahead of the company’s next earnings call.1

That is why I thought Cook’s most telling phrase was “How Important These Services Are For Us”; if Cook wanted to signify how importantly Apple was taking its efforts in developing these services, “to us” would have been a more natural turn of phrase. And, while I grant that is probably what Cook meant, the preposition change, in my estimation, gets at the heart of the matter: the iPhone isn’t going anywhere — Apple is very much not doomed — but it is no longer growing, leaving Apple no choice but to look elsewhere.

There are, broadly speaking, three ways that already big companies like Apple, cash cows like the iPhone in hand, can achieve growth:

Create New Products: This is the most obvious path, and also the most difficult. Creating products that resonate is really hard.

Still, that hasn’t stopped Apple from trying, and frankly, the company is doing quite well: the Apple Watch is a hit, AirPods are becoming a cultural phenomena (and the potential foundation for audio-based augmented reality), and the company is well-placed to compete in the visual-based augmented reality space. The HomePod is a bit of a dud, but to management’s credit the company appears to have already moved on. All of these successful products fit Apple’s DNA of personal computing, and are the most encouraging signals that Apple will be fine.

The problem, though, is that there will never be a product like the iPhone again; Apple may have found its product future (good for developers and customers), but its financial future is less certain (not so good for Wall Street).

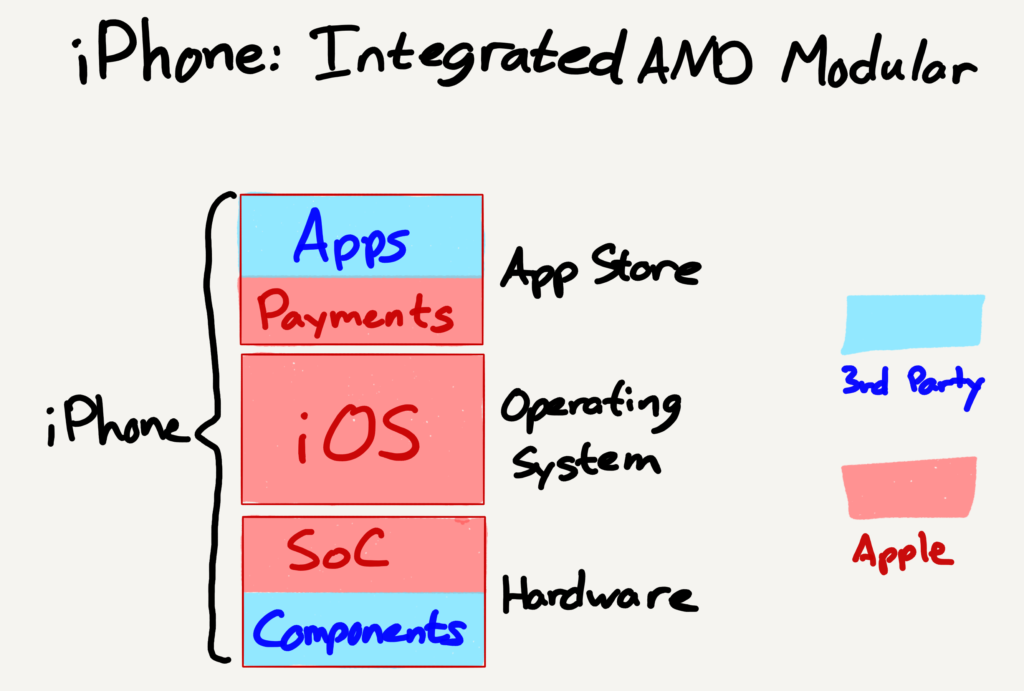

Extend Integration: Apple is, famously, vertically integrated; the company writes the software that differentiates the iPhones that it manufactures and sells for a profit. That does not mean, though, that the entire iPhone experience is integrated — there are significant amounts of modularity. For example, Apple sources nearly all iPhone components from 3rd-party suppliers (Samsung, to take a counter example, manufactures more of its own components), and of course the vast majority of apps that are used on iPhones are made by 3rd-parties as well.

However, Apple can and has extended its integration into areas that were previously modular. On the component side, Apple started selling devices with processors it designed for its exclusive use in 2010, very successfully increasing iPhone differentiation in terms of performance. And, on the App side, Apple from the beginning of the App Store integrated forward into payments, and has extended that integration through App Store rules. I illustrated these integrations in a 2015 article entitled Apple’s New Market:

Apple has also integrated Services like iCloud backup, Siri, and Photo Stream; those services, though, have been more akin to Apple’s integration into processors in that said services are meant to differentiate iPhones, not be revenue drivers in their own right.

Yesterday’s announcements were an important departure from that strategy in two respects. First, services like Apple Card, Apple Arcade, and Apple News+ (I will get into the details of these services later on) extend Apple’s integration forward with the goal of driving new revenue.

Previously games in the App Store were sold individually; Apple Arcade relies on Apple’s control of the App Store (and the fact the company does not need to pay itself 30%) to create a new bundle

Previously news and magazine apps could be subscribed to individually; Apple News+ relies on Apple’s control of the App Store (and the fact the company does not need to pay itself 30%) to create a new bundle

Secondly, Apple also announced at least one service — Apple TV+ — that…well, it’s not quite clear to what extent it is an extension as opposed to a new product entirely. But, before I explore the implications of that distinction, it’s worth calling out the last avenue for growth:

Acquisitions: This is, by definition, the most expensive way to acquire growth. It is also often the one that makes the most sense for cash-generating behemoths like Apple — and exploring the prospects of Apple TV+ show why.

The Apple TV portion of yesterday’s announcement actually had two parts: the Apple TV+ streaming service, which I will get to in a moment, and Apple TV Channels. The latter is a service akin to Amazon Channels or the Roku Channel Store; customers can subscribe to a la carte “channels” like HBO or Showtime, the content of which will be incorporated into the Apple TV app.

If this sounds familiar it is because this is Apple’s second version of this concept (this time Apple hosts the streams and controls the player, as opposed to relying on 3rd-party apps); the first version was announced in October, 2016, and then, as is the case now, Netflix, whose management claims it accounts for 10% of all TV time in the US, was not included. I explained why at the time:

Apple’s desire to be “the one place to access all of your television” implies the demotion of Netflix to just another content provider, right alongside its rival HBO and the far more desperate networks who lack any sort of customer relationship at all. It is directly counter to the strategy that has gotten Netflix this far — owning the customer relationship by delivering a superior customer experience — and while Apple may wish to pursue the same strategy, the company has no leverage to do so. Not only is the Apple TV just another black box that connects to your TV (that is also the most expensive), it also, conveniently for Netflix, has a (relatively) open app platform: Netflix can deliver their content on their terms on Apple’s hardware, and there isn’t much Apple can do about it.

That article, by the way, was entitled Apple Should Buy Netflix: I argued that iPhone growth was on the verge of slowing, that Apple needed a new growth driver to give the company space to create new products, and that the company was uniquely suited to provide Netflix’s biggest need — cash — which actually wasn’t doing Apple itself much good:

Apple is at its best when it is creating new products that are the best they can possibly be; it is a capability that is rather independent from Apple’s biggest strategic assets: its dedicated user base and massive cash pile.

Instead Apple has decided to compete with Netflix, at least to an extent, using those strategic assets: the company is spending some billions of dollars to create original content that will be available on all Apple devices. Notably, though, Apple TV+ content will be available on other devices as well, including Amazon and Roku’s TV boxes and smart TVs from Samsung, LG, Sony, and Vizio.

It appears that Apple is attempting to thread the finest of needles: by not having players available on Android, Windows, or the web, Apple TV+ acts as another extension of Apple’s integrated model, differentiating Apple’s hardware in the process. The problem, though, is that creating or acquiring content is a fixed cost: that means that the economically optimal approach is to make that content available as widely as possible, increasing leverage on those fixed costs. Thus the partnerships with Amazon, Roku, and smart TV manufacturers.

Unfortunately for Apple, I’m not sure that this exclusion is sustainable when it comes to competing with Netflix. As demonstrated by the parade of celebrities during the second half of yesterday’s event, Hollywood is driven first-and-foremost by cash. Whoever pays more for a show gets that show, even if — as Netflix continues to demonstrate — the entity making the payment is in the process of upending the entire TV value chain.

To that end, Apple certainly has the cash to compete with Netflix on a show-by-show basis (thanks to the still fabulously popular and profitable iPhone in particular); what is critical to understand, though, is that outbidding Netflix for a show basically guarantees that said show will lose money for Apple, at least for the next few years, thanks to Netflix’s huge subscriber base.

The challenge for Apple goes back to the leverage point I mentioned above. Consider a drastically simplified example:

Netflix’s break-even point for a show is $2,000 (200 x $10); sure, Apple could outbid Netflix and pay $2001, but that means a loss of $1501 ($2001 – (50 x $10)). Is Apple willing to stomach the years of losses necessary to increases its subscriber base to a level where it can profitably compete with Netflix for shows? And, as a short-term concern, can Apple really afford to ignore billions of Android and Windows devices?

Indeed, this is precisely why I argued that Apple should simply acquire Netflix back when the company was worth <$50 billion (the price tag is quite a bit more unrealistic now);2 truly competing in the streaming video space, with its horizontal model that works orthogonally to Apple’s core vertical business model, means that the only real advantages Apple has are the default apps on the iPhone and a huge amount of cash, and those advantages could be applied to an acquired Netflix far more efficiently than they could to a brand new streaming service — like Apple TV+.

That, though, takes me back to the needle Apple appears to be trying to thread: the only way that Apple TV+ makes sense strategically is not as a new product with a new business model, but rather as another extension of Apple’s integration, i.e. a way to not simply sell new iPhones but also Apple’s TV app generally, including the commissions Apple will collect from Apple TV channels.

In short, Apple may increasingly be a services company in terms of the recurring revenue it earns, but its strategy is still very much rooted in a product world where differentiation comes from vertical integration.

A few additional notes about the other services Apple announced:

Apple Card: This makes a ton of sense: Apple is uniquely placed to differentiate a credit card thanks to Apple Wallet and Apple Pay (a numberless card is particularly neat, and only possible because of the Apple Wallet integration); the rewards and interest rates are very average (in-line with the Amazon Rewards Visa but inferior to the Amazon Prime Rewards Visa) but, in true Apple fashion, the card is much cooler looking. Also, don’t be surprised that Apple is partnering with Goldman Sachs: the company (rightly) wants nothing to do with the regulations entailed by being a bank, even if it means sharing those lucrative transaction fees.

Apple Arcade: This will hurt the up-front purchase game market, at least what little is left of it. The most reliable way to make money in the App Store is with either a free-to-play model (where you have to buy in-app purchases to progress) or a free-to-win model (where in-app purchases are largely aesthetic, a la Fortnite). Games that support neither are left trying to adapt Apple’s in-app purchase mechanism to support trials (i.e. download the game for free, make two levels free, and make an in-app purchase to unlock the rest) and praying their game will be featured in the App Store so that they can recoup their costs.

Apple Arcade is a very different model: first, Apple is paying up-front for exclusivity — already a more sustainable model for game developers — and second, subscribers (i.e. people who are generally willing to try and buy new games regularly) will surely look to try other Apple Arcade games before they bother downloading new ones, making things tough for anyone not a part of the bundle. Again, though, it is not as if the current situation is great for traditional games that you pay once for anyways; there is a decent chance this is a more sustainable model for everyone (and, of course, a nice revenue stream for Apple).

Apple News+: This slide transition neatly encapsulates both the devastation wracked on the media by the Internet as well as why Apple can take 50% of every Apple News+ subscription:

The vast majority of media is completely commoditized and, in a world of zero marginal costs, happy to accept whatever pennies Apple is willing to throw their way. What is more noteworthy are the publications that aren’t there, particularly newspapers that have managed to develop direct connections with customers based on subscriptions (and one that is — the Wall Street Journal — is severely limited in discoverability and availability). This is exactly the right decision for them, as I explained last month in The Cost of Apple News.

That leaves Cook’s final line: At Apple, the customer is, and always will be, at the center of everything that we do.

Frankly, with the possible exception of Apple Arcade, it is hard to see this sentiment in yesterday’s announcements; I’m not saying any of these services are customer hostile, but most of them are imitations of what other companies are already doing, the revenues of which Apple wants a cut of. And that’s okay: a growing Apple is better placed to build the next great product that changes customers’ lives. Still, I can’t help but think of a famous Steve Jobs quote:

I want to put a ding in the universe. Your time is limited, so don’t waste it living someone else’s life. Don’t be trapped by dogma — which is living with the results of other people’s thinking.

Yesterday didn’t have many dings, and fair bit of other people’s business models. Only time will tell if the diversion from what the company does best leaves Apple trapped.

I wrote a follow-up to this article in this Daily Update.

On Exponent, the weekly podcast I host with James Allworth, we discuss Where Warren’s Wrong.

Listen to it here.

Senator Elizabeth Warren deserves credit: I have been writing about antitrust, particularly in the context of Aggregation Theory, for years, but the most concrete proposal I have put forward is that social networks should not be allowed to acquire other social networks. Senator Warren, on the other hand, last week presented a far more wide-reaching proposal that specifically targeted Facebook, Google, and Amazon:

Today’s big tech companies have too much power — too much power over our economy, our society, and our democracy. They’ve bulldozed competition, used our private information for profit, and tilted the playing field against everyone else. And in the process, they have hurt small businesses and stifled innovation.

I want a government that makes sure everybody — even the biggest and most powerful companies in America — plays by the rules. And I want to make sure that the next generation of great American tech companies can flourish. To do that, we need to stop this generation of big tech companies from throwing around their political power to shape the rules in their favor and throwing around their economic power to snuff out or buy up every potential competitor.

That’s why my administration will make big, structural changes to the tech sector to promote more competition — including breaking up Amazon, Facebook, and Google.

Senator Warren added Apple in an interview at SXSW with The Verge:

There was one company that fits that description that you did not mention.

Apple. They’re in.

You want to break up Apple as well.

Yep.

You were very specific about how you’d break up Google and the rest. How would you break up Apple?

Apple, you’ve got to break it apart from their App Store. It’s got to be one or the other. Either they run the platform or they play in the store. They don’t get to do both at the same time. So it’s the same notion.

Unfortunately, Senator Warren’s proposal helps highlight why I have not gone further with my own: hers would create massive new problems, have significant unintended consequences, and worst of all, not even address the issues Senator Warren is concerned about (with one possible exception I will get to in a moment). Worst, it would do so by running roughshod over the idea of judicial independence, invite endless lawsuits and bureaucratic meddling around subjective definitions, and effectively punish consumers for choosing the best option for them. Mike Masnick at TechDirt gets into many of these problems, and concludes:

This entire plan gets headlines (duh) because so many people are (perhaps reasonably!) angry at the power of big tech companies. But, very little in the actual plan makes much sense. The “platform utility” idea will lead to massive, wasteful, stupid lawsuits. The unwinding of old mergers will involve interfering with an independent agency, and seem unlikely to do much to change the main “concerns” that Senator Warren raises in the first place.

And, again, none of this is to say we shouldn’t be concerned about big internet companies with too much power. It’s a perfectly reasonable concern, but just because you want to “do something” and “this is something,” doesn’t mean that it’s the something we should do.

I do know what is the first thing Senator Warren should do: rectify three clear areas where I believe she is mistaken about technology. Her proposal is wrong about tech’s history, the source of the tech giants’ power, and the fundamental nature of technology itself. All three are, unsurprisingly, interrelated, and it is impossible to craft a cogent antitrust policy without getting all of them right.

Senator Warren opens the article by crediting the Microsoft antitrust case for the emergence of Google and Facebook:

Twenty-five years ago, Facebook, Google, and Amazon didn’t exist. Now they are among the most valuable and well-known companies in the world. It’s a great story — but also one that highlights why the government must break up monopolies and promote competitive markets.

In the 1990s, Microsoft — the tech giant of its time — was trying to parlay its dominance in computer operating systems into dominance in the new area of web browsing. The federal government sued Microsoft for violating anti-monopoly laws and eventually reached a settlement. The government’s antitrust case against Microsoft helped clear a path for Internet companies like Google and Facebook to emerge.

The story demonstrates why promoting competition is so important: it allows new, groundbreaking companies to grow and thrive — which pushes everyone in the marketplace to offer better products and services. Aren’t we all glad that now we have the option of using Google instead of being stuck with Bing?

Start with the most obvious error: Bing was not even launched until 2009, eight years after the Microsoft case was settled. MSN Search, its predecessor, did launch in 1998, but with licensed search results from Inktomi and AltaVista; Microsoft didn’t launch its own web crawler until 2005 (these details will matter in a moment).

What is more striking is that, in retrospect, the core piece of the government’s case doesn’t make any sense: of course a browser should be bundled with an operating system; a new computer without a browser would be practically useless (for one, how do you install a browser?). Moreover, Apple, not without merit, argues that restricting rendering engines to the one that ships with the OS (all browsers on iOS have no choice but to use the built-in rendering engine) has significant security benefits; this is debatable, but ultimately, most don’t care, simply because browsers are means to information, not ends.

This, crucially, is something Microsoft did not understand in the 1990s; Microsoft’s operating system monopoly was predicated on owning the APIs with which applications were built, creating both lock-in and an ever expanding network effect. Unsurprisingly, Microsoft viewed the web through this exact same lens; that meant that Netscape was a threat because it was “middleware”, a potential means to run applications that were not locked into Windows. This is true, by the way — web apps work across operating systems and browsers — but this fact has absolutely nothing to do with the rise of Google. After all, when Google IPO’d in 2004, Internet Explorer had 95% market share; a browser was a means, not an end.

The reality is that Google is an operating system of sorts, but the system is not a PC but rather the entire web; what ties things together are not APIs, but links. And, crucially, the business model that makes sense is not licensing, but advertising. This is a value chain that never even occurred to Microsoft, and why would it? The entire company was predicated on controlling operating systems for physical computers, controlling the APIs on top, and earning revenue through licensing; it was fabulously profitable, and as history shows again and again, being fabulously profitable with an existing value chain is the best way to not only fail to recognize a new market opportunity (Microsoft didn’t even have a web crawler until after Google’s IPO!), but to in fact be at a massive disadvantage when you finally do so.

Look no further than mobile: Microsoft was not encumbered by antitrust when it came to their mobile ambitions, and yet they failed even more spectacularly there than they did online. In this case the company didn’t “miss” the opportunity — Windows Mobile came out back in 2000 — it was just stuck in a PC mindset when it came to product development, attached to its Windows licensing model when it came to monetization, and institutionally incapable of producing superior end user experiences thanks to the company’s traditional focus on platforms and compatibility.

In short, to cite Microsoft as a reason for antitrust action against Google in particular is to get history completely wrong: Google would have emerged with or without antitrust action against Microsoft; if anything the real question is whether or not Google’s emergence shows that the Microsoft lawsuit was a waste of time and money.1

Senator Warren’s second mistake is a misstating of why large tech companies are dominant. She writes:

America’s big tech companies have achieved their level of dominance in part based on two strategies:

Using Mergers to Limit Competition. Facebook has purchased potential competitors Instagram and WhatsApp. Amazon has used its immense market power to force smaller competitors like Diapers.com to sell at a discounted rate. Google has snapped up the mapping company Waze and the ad company DoubleClick. Rather than blocking these transactions for their negative long-term effects on competition and innovation, government regulators have waved them through.

Using Proprietary Marketplaces to Limit Competition. Many big tech companies own a marketplace — where buyers and sellers transact — while also participating on the marketplace. This can create a conflict of interest that undermines competition. Amazon crushes small companies by copying the goods they sell on the Amazon Marketplace and then selling its own branded version. Google allegedly snuffed out a competing small search engine by demoting its content on its search algorithm, and it has favored its own restaurant ratings over those of Yelp.

The merger issue is a real one, but only when it comes to propagating power; Facebook was dominant before it bought Instagram and WhatsApp, Google before it bought DoubleClick or YouTube, and Amazon before it bought Diapers.com or Whole Foods (I do share Senator Warren’s concern about acquisitions; I will return to this point). Notably, Apple has not made any major acquisitions other than Beats headphones, and that too came well after the company had created the iPhone.

Similarly, the conflict of interest Senator Warren worries about is also post-dominance; none of Google, Facebook, Amazon, nor Apple achieved their power by “using proprietary marketplaces to limit competition”. That is not to say this, like acquisitions, isn’t a worthwhile issue, but it is flat out wrong to say that these are the reasons “big tech companies achieved their level of dominance.”

Then again, perhaps it is best for Senator Warren’s argument that her article never does explain how these companies became so big, because the reason cuts at the core of her argument: Google, Facebook, Amazon, and Apple dominate because consumers like them. Each of them leveraged technology to solve a unique user needs, acquired users, then leveraged those users to attract suppliers onto their platforms by choice, which attracted more users, creating a virtuous cycle that I have christened Aggregation Theory. Specifically:

Aggregation Theory is the reason why all of these companies have escaped antitrust scrutiny to date in the U.S.: here antitrust law rests on the consumer welfare standard, and the entire reason why these companies succeed is because they deliver consumer benefit.

The European Union does have a different standard, rooted in a drive to preserve competition; given that the virtuous cycle described by Aggregation Theory does tend towards winner-take-all effects, it is not a surprise that Google in particular has faced multiple antitrust actions from the European Commission. Even the EU standard, though, struggles with the real consumer benefits delivered by Aggregators.

Consider the Google Shopping case: Google was found guilty of antitrust violations in a case brought by a shopping comparison site called Foundem, which complained about their site being buried when consumers were searching for items to buy. This complaint made no sense, as I explained in Ends, Means, and Antitrust:

If I search for a specific product, why would I not want to be shown that specific product? It frankly seems bizarre to argue that I would prefer to see links to shopping comparison sites; if that is what I wanted I would search for “Shopping Comparison Sites”, a request that Google is more than happy to fulfill:

The European Commission is effectively arguing that Google is wrong by virtue of fulfilling my search request explicitly; apparently they should read my mind and serve up an answer (a shopping comparison site) that is in fact different from what I am requesting (a product)?

There is certainly an argument to be made that Google, not only in Shopping but also in verticals like local search, is choking off the websites on which Search relies by increasingly offering its own results. At the same time, there is absolutely nothing stopping customers from visiting those websites directly, or downloading their apps, bypassing Google completely. That consumers choose not to is not because Google is somehow restricting them — that is impossible! — but because they don’t want to. Is it really the purview of regulators to correct consumer choices willingly made?

As I noted above, there are some important points made here by Senator Warren; at a fundamental level, though, any sort of antitrust proposal that does not seriously grapple with the reality that the power of these companies flows from controlling demand — that is, consumer choice, willingly made — not from controlling supply, like monopolies of old, is going to be fundamentally flawed.

This mistake by Senator Warren only came into focus with that interview where she included Apple as a target for her proposal. Here’s more from that interview:

Pulling that apart, the App Store is the method by which Apple keeps the iPhone secure. It’s integrated into the platform. How would you propose that Apple and Google distribute apps if they don’t run the store?

Well, are they in competition with others who are developing the products? That’s the problem all the way through this, and it’s what you have to keep looking for. If you run a platform where others come to sell, then you don’t get to sell your own items on the platform because you have two comparative advantages. One, you’ve sucked up information about every buyer and every seller before you’ve made a decision about what you’re going to sell. And second, you have the capacity — because you run the platform — to prefer your product over anyone else’s product. It gives an enormous comparative advantage to the platform.

This would not be the first time in US history that this kind of arrangement had to be broken up. Back when the railroads were dominant, and you had to get steel or wheat onto the railroad, there was a period of time when the railroads figured out that they could make money not only by selling tickets on the railroad, but also by buying the steel company and then cutting the price of transporting steel for their own company and raising the price of transporting steel for any competitors. And that’s how the giant grows.

The problem is that’s not competition. That’s just using market dominance, not because they had a better product or because they were somehow more customer-friendly or in a better place. It’s just using market dominance. So my principle is exactly the same: what was applied to railroad companies more than a hundred years ago, we need to now look at those tech platforms the same way.

This is pretty explicitly taking Senator Warren’s critique of Amazon in particular and applying it to Apple, and to be fair, it is not completely without merit: Apple has quite clearly leveraged the fact it owns the platform to compete with Spotify, for example, and has definitely suppressed competition when it comes to built-in apps like Mail and the aforementioned Safari.

At the same time, do consumers not matter at all here? Is Senator Warren seriously proposing that smartphone be sold with no apps at all? Was Apple breaking the law when they shipped the first iPhone with only first-party apps? At what point did delivering an acceptable consumer experience out-of-the-box cross the line into abusing a dominant position? This argument may make sense in theory but it makes zero sense in reality.

What is even more striking, though, is that the App Store does have a massive antitrust problem: it is not Apple unfairly competing with app developers, it is Apple unfairly imposing massive complexity and extracting 30% of revenue with its contractual requirement, enforced by App Review, that developers use Apple’s payment mechanism. I wrote about this extensively last year in Antitrust, the App Store, and Apple (also see this follow-up); I think there is a case Apple’s policies would be found anticompetitive under a Quick Look review, and may even be a per se antitrust tying violation.

The important takeaway for this Article, though, is the degree to which Senator Warren missed the point: there is significant consumer benefit both to having preinstalled apps and also to Apple controlling the installation of apps. There is a big benefit to suppliers (app developers) as well: the app market on PCs died in large part due to security concerns, which Apple obviated with the App Store to the tremendous benefit of every participant in the ecosystem. Senator Warren’s proposal would make the App Store worse for everyone.

That leads to a broader point: “tech” is not simply another category, like railroads or telecom. Tech is a means, not an end, but Senator Warren’s approach presumes the latter. That is why she proposes the same set of rules for the sale of toasters and the sale of apps, and everything in between. The truth is that Amazon is a retailer; Apple a combination of hardware maker and platform makers. Google is a search and advertising company, and Facebook a publishing and advertising company. They all have different value chains and different ways of impacting competition, both fairly and unfairly, and to fail to appreciate just how different they are is a great way to make bad laws that not only fail to fix problems but also create entirely new ones.

That is not to say there aren’t genuine concerns about the biggest tech companies; I was absolutely genuine when I stated at the beginning that Senator Warren deserves credit for bringing these issues to the forefront. To my mind there are three major issues that deserve antitrust attention:

Senator Warren expresses concern in her article about kill zones when it comes to new startups:

Weak antitrust enforcement has led to a dramatic reduction in competition and innovation in the tech sector. Venture capitalists are now hesitant to fund new startups to compete with these big tech companies because it’s so easy for the big companies to either snap up growing competitors or drive them out of business. The number of tech startups has slumped, there are fewer high-growth young firms typical of the tech industry, and first financing rounds for tech startups have declined 22% since 2012.

This is decidedly not the case when it comes to enterprise-focused startups: that sector is thriving with all kinds of new businesses being created, acquired, and going public. The problem is the consumer Internet, which is to say that the problem is digital advertising. As I explained last year, both Google and Facebook are Data Factories; writing about Facebook specifically:

Facebook quite clearly isn’t an industrial site (although it operates multiple data centers with lots of buildings and machinery), but it most certainly processes data from its raw form to something uniquely valuable both to Facebook’s products (and by extension its users and content suppliers) and also advertisers (and again, all of this analysis applies to Google as well):

- Users are better able to connect with others, find content they are interested in, form groups and manage events, etc., thanks to Facebook’s data.

- Content providers are able to reach far more readers than they would on their own, most of whom would not even be aware those content providers exist, much less visit of their own volition.

- Advertisers are able to maximize the return on their advertising dollar by only showing ads to individuals they believe are predisposed to like their product, making it more viable than ever before to target niches (to the benefit of their customers as well).

And then, in exchange for these benefits that derive from data, Facebook sucks in data from all three entities:

- Users provide Facebook with data directly, both through information and media they upload, and also through their actions on Facebook properties.

- Content is not simply data in its own right, but also a catalyst for generating user action data.

- Advertisers, like content providers, not only provide data in its own right, which acts as a catalyst for generating user action data, but also upload huge amounts of data directly in order to better target prospective customers.

The end result is that Facebook and Google are far more valuable to advertisers than anyone else: they offer the most efficient spend when it comes to a return on advertising, and thanks to their ability to reach practically everyone, combined with the infinite nature of digital content, require the lowest investment. Put plainly, the ROI on Google and Facebook digital advertising is unmatched, and the chasm is only growing.

This is a tremendous problem for any would-be consumer Internet company, particular any product that depends on a network effect. The single most important feature when it comes to building a large user base and a leverage-able network effect is that the product be free-to-use, which means the only viable business model is advertising. As I just noted, though, the only place that advertisers want to be — for good reason! — is Google or Facebook. Ergo, consumer Internet companies are increasingly difficult to get started.

Snap is an unfortunate example of this reality: Snapchat is a clear demonstration that it is possible to build a competing social network in a world dominated by Facebook; unfortunately, it also appears to be an example of how is is even more difficult to build a profitable advertising business.

I don’t have a clear solution to this problem; if anything, privacy-focused regulation like GDPR are only exacerbating the issue, given that Google and Facebook acquire most user data on their platforms. Any solution that seeks to actually make a positive impact on competition, though, has to start with advertising.

As I’ve hinted at a couple of times in this article, this is where I do mostly agree with Senator Warren. The truth is that Snapchat would have been a far greater threat to Facebook had the latter not been allowed to acquire Instagram. In a Daily Update last year I explored an alternate history where Instagram stayed independent:

This is where it is critical to consider the entire ecosystem. Had Instagram continued as a standalone company I do believe it would have been successful in building out an advertising business; it just would have taken a lot more time and effort…What is more important, though, is that an independent Instagram would have been the best possible thing that could have happened to Snapchat. The fundamental problem facing Snapchat is that it wasn’t enough for the company to have higher usage or deeper engagement with teens and young adults, demographic groups advertisers are desperate to reach. As long as Instagram was using Facebook’s ad infrastructure, it would always be more cost effective to reach those groups using Facebook’s ad engine.

This is why I have called Facebook’s acquisition of Instagram The Greatest Regulatory Failure of the Past Decade, and called for an end to social networks being allowed to buy other social networks. I do have qualms about the idea of retroactively undoing deals, but I do think Senator Warren is directionally correct in this case.

More broadly, as I explained in The Value Chain Constraint, the price of being an Aggregator is tuning your company to the value chain within which you compete; it follows that all of these companies will face significant challenges moving into new spaces with new value chains. To that end, what makes the most sense from a management perspective is leveraging the tremendous amounts of cash thrown off by their core businesses to acquire and invest in companies competing in different value chains.

On the flipside, to the extent regulators wish to constrain Aggregators, the single most effective lever is limiting acquisitions. There are significant problems with this, to be sure, particularly when it comes to the incentives for new company creation (most successful exits are acquisitions, not IPOs), but at least this is a remedy that is somewhat approaching the problem.

As I have detailed, Aggregators already have massive structural advantages in their value chains; to that end, there should be significantly more attention paid to market restrictions that are enforced by contracts.

Go back to Microsoft: in my estimation the most egregious antitrust violations committed by Microsoft were the restrictions placed on OEMs, both to ensure the installation of Internet Explorer as well as to suppress alternative operating systems. These were not violations rooted in market dominance, at least not directly, but rather contracts that OEMs could not afford to say ‘No’ to.

This is an area where the European Commission has gotten it right with regard to Google: as a condition of access to Google apps, most critically the Play Store, OEMs were prohibited from selling any phones with Android forks. This is a restriction on competition produced not by market dominance, at least not directly, but rather contracts that OEMs could not afford to say ‘No’ to.

This is also the issue with Apple’s App Store: the restriction on linking to a website for purchasing an ebook or subscribing to a streaming service is not rooted in any sort of technical limitation; rather, it is an arbitrary rule in the App Developer Agreement enforced by Apple’s App Review team. It has nothing to do with consumer security, and everything to do with Apple’s bottom line.

This is an area ripe for enhanced antitrust enforcement: these large tech companies have enough advantages, most of them earned through delivering what customers want, and abetted by the fundamental nature of zero marginal costs. Seeking to augment those advantages through contracts that suppliers can’t say ‘No’ to should be viewed with extreme skepticism.

Let me reiterate a point I have made twice now: I appreciate Senator Warren raising these issues; they are indeed critical not only for the world today, but also the world we wish to create in the future. That, though, only increases the importance of getting things right: the history, the fundamental problem, and the nature of tech. Only then can we start to grope for solutions that actually make the situation better rather than worse.

I wrote a follow-up to this article in this Daily Update.

In short, while there are arguments to be made about the impact of the antitrust decision on the emergence of web apps — which again, was Microsoft’s core concern — it has nothing to do with the emergence of Google, which was not only not competitive with Microsoft but not even on the company’s radar at the time of the antitrust case. [↩]

On Exponent, the weekly podcast I host with James Allworth, we discuss Facebook’s Privacy Cake.

Listen to it here.

What was striking about the reaction to Mark Zuckerberg’s latest missive about the future of Facebook, A Privacy-Focused Vision for Social Networking, were the two very distinct reactions that, in my estimation, made the same mistake, but in opposite directions; one set of folks didn’t take Zuckerberg seriously at all:

Mark Zuckerberg today: ”I believe we should be working towards a world where people can speak privately and live freely knowing that their information will only be seen by who they want to see it.” How long has he personally believed this? An hour? A day? https://t.co/2qmZjl8Iaq

— Walt Mossberg (@waltmossberg) March 6, 2019

Another set took Zuckerberg entirely too seriously:

I am not a stock market person but the fact that Facebook’s stock hardly budged on a day that Mark Zuckerberg said he planned to pivot the company to a totally untested new business model seems odd to me

— Casey Newton (@CaseyNewton) March 7, 2019

In fact, what Zuckerberg announced is quite believable, precisely because it makes perfect sense for Facebook: this is a privacy cake that Facebook can have — and eat it too.

Zuckerberg began by describing two distinct kinds of social networks:

Over the last 15 years, Facebook and Instagram have helped people connect with friends, communities, and interests in the digital equivalent of a town square. But people increasingly also want to connect privately in the digital equivalent of the living room. As I think about the future of the internet, I believe a privacy-focused communications platform will become even more important than today’s open platforms. Privacy gives people the freedom to be themselves and connect more naturally, which is why we build social networks.

Today we already see that private messaging, ephemeral stories, and small groups are by far the fastest growing areas of online communication. There are a number of reasons for this. Many people prefer the intimacy of communicating one-on-one or with just a few friends. People are more cautious of having a permanent record of what they’ve shared. And we all expect to be able to do things like payments privately and securely.

Public social networks will continue to be very important in people’s lives — for connecting with everyone you know, discovering new people, ideas and content, and giving people a voice more broadly. People find these valuable every day, and there are still a lot of useful services to build on top of them. But now, with all the ways people also want to interact privately, there’s also an opportunity to build a simpler platform that’s focused on privacy first.

I first explored the idea of there being different types of social networks in 2013 when I created The Social/Communications Map:

Keep in mind, this image is from 2013, but there are still some important points worth calling out:

The most important thing to note, though, are the relative positions of Facebook and Snapchat (it was Facebook’s attempted acquisition of Snapchat that inspired the map in the first place).

Perhaps the most important moment in Facebook’s history was its shift from the private to public space on the Social/Communications Map with the introduction of the News Feed. Again, to be clear, this map is about public perception, not technical reality, and this is a perfect example: data on Facebook was public to everyone in your network from day one. What the News Feed did, though, was change Facebook data from a pull to a push model: instead of needing to seek out your friends’ profiles Facebook would push their updates to you directly.

This inspired a strong backlash amongst users, who not only complained online but actually organized rallies in person; ultimately, though, it turned out that people loved the News Feed, and once Facebook embraced mobile, it turned out the News Feed was perfect for advertising.

Still, that transition exposed a soft underbelly in Facebook’s product: private ephemeral communication that allowed users to be their true selves. This was the premise undergirding Snapchat, which I described in Facebook, Phones, and Phonebooks:

It is increasingly clear that there are two types of social apps: one is the phone book, and one is the phone. The phone book is incredibly valuable: it connects you to anyone, whether they be a personal friend, an acquaintance, or a business. The social phone book, though, goes much further: it allows the creation of ad hoc groups for an event or network, it is continually updated with the status of anyone you may know or wish to know, and it even provides an unlimited supply of entertaining professionally produced content whenever you feel the slightest bit bored.

The phone, on the other hand, is personal: it is about communication between you and someone you purposely reach out to. True, telemarketing calls can happen, but they are annoying and often dismissed. The phone is simply about the conversation that is happening right now, one that will be gone the moment you hang up.

In the U.S. the phone book is Facebook and the phone is Snapchat; in Taiwan, where I live, the phone book is Facebook and the phone is LINE. Japan and Thailand are the same, with a dash of Twitter in the former. In China WeChat handles it all, while Kakao is the phone in South Korea. For much of the rest of the world the phone is WhatsApp, but for everywhere but China the phone book is Facebook.

Make no mistake, the phonebook has been more valuable: it lends itself better to both data collection and advertising. Snapchat, though, threatened to break out of the phone space into the phonebook space with Stories — a product that shifted Snapchat out of the private space into the public one.

To that end, it is instructive that it is Stories where Facebook finally mounted its Snapchat defense: I wrote in The Audacity of Copying Well:

Instagram and Facebook are smart enough to know that Instagram Stories are not going to displace Snapchat’s place in its users lives. What Instagram Stories can do, though, is remove the motivation for the hundreds of millions of users on Instagram to even give Snapchat a shot.

That is exactly what happened: Snap retained its place as the core of 1×1 communication for young people, but the segments more removed from Snapchat’s core use case of chat were suddenly far less likely to even give the service a try, thanks to Instagram’s intelligent leveraging of its network.

By the same token, though, just because Facebook capped Snapchat’s growth doesn’t mean that Snapchat’s core insight about the desire for private, ephemeral communication was wrong: what Zuckerberg wrote yesterday is basically Snapchat’s reason-for-existing. In other words, while Instagram Stories built a wall around Snapchat by copying Snapchat’s secondary feature, this “Privacy-Focused Vision for Social Networking” is a clear attempt to build the core of Snapchat for everyone else.

Look again at what Zuckerberg outlined:

The first three are all about owning the 1×1 private ephemeral space; critically, none of them have anything to do with Facebook’s core feed-based products. Facebook is going to continue to exist as it has to date, as will Instagram, including all of the data collection and ad targeting that currently exist. The “Privacy-Focused Vision for Social Networking” is in addition to Facebook’s current products, not in place of. This is the mistake made by those that took Zuckerberg too seriously.

As for those who didn’t take Zuckerberg seriously enough, why wouldn’t Facebook want to move in this direction? There are multiple benefits:

Perhaps most compelling, though, is the degree to which this move locks in Facebook’s competitive position. As I noted above, Snapchat already showed that Facebook is vulnerable in the realm of private ephemeral communications, but soon that will no longer be the case. Moreover, given Facebook’s focus on end-to-end encryption, the company has made it that much harder to even get off the ground: not even Snapchat is fully end-to-end encrypted (pictures are, but not text messages).

There is an even more important benefit to Facebook voluntarily forgoing the data within messages and limiting the time it keeps surrounding metadata (make no mistake, end-to-end encryption is a real thing — Facebook will not be able to see encrypted messages); as Zuckerberg told Wired:

Certainly, ad targeting can benefit from having access to as much content or signal as possible. You know, I’m more optimistic about this for a few reasons. One is that we aren’t really using the content of messages to target ads today anyway. So we weren’t planning on doing that. So it’s not like building a system and making it end-to-end encrypted and now we can’t see the messages is really going to hurt ads that much because of the way we were already thinking about that. Keeping metadata around for less time will have some impact, although I’m optimistic that we’ll build systems that can basically deliver most of the value with a fraction of the amount of data.

Why can Facebook deliver most of the value? Because they are still Facebook! They still have the core Facebook app, Instagram, ‘Like’-buttons scattered across the web — none of that is going away with this announcement. They can very much afford a privacy-centric messaging offering in a way that any would-be challenger could not. Privacy, it turns out, is a competitive advantage for Facebook, not the cudgel the company’s critics hoped it might be.

The last three items in Zuckerberg’s list are interesting in their own right; to take them one-by-one:

Safety: This is about the very real trade-offs that come with end-to-end encryption. One obvious issue is law-enforcement: Apple has already been down this road with the FBI when it comes to phone security; end-to-end encryption is both more challenging and yet simpler, simply because it is, properly implemented, truly unbreakable.

Another issue is misinformation: for all of the issues surrounding misinformation on Facebook, at least misinformation is traceable; that is not the case if messages are encrypted, which has already been an issue with WhatsApp in India. One could certainly make the cynical argument that, in the process of cloaking itself in privacy, Facebook is washing its hands of misinformation.

To be sure, Facebook is confident it can leverage its ability to analyze metadata to stop bad actors; that the exact same sort of audience analysis is perfectly portable to advertising is a rather happy benefit as far as Facebook is concerned.

Interoperability: This is perhaps the feature that is easiest to be cynical about; while it can certainly be frustrating to have to balance multiple messaging apps, for much of the world consolidating Facebook-owned messaging will not fully address the problem, thanks to alternatives like Messages, LINE, Kakao, etc. Moreover, even in areas where Facebook owns both the Phone (via WhatsApp) and the phonebook (via Facebook and Instagram), exactly how much consumer demand is there for integration?

There is, to be sure, a business argument: Facebook has already unified much of the ad infrastructure underlying its services, and unifying messaging is, to the extent Facebook wants to build a business platform on messaging, a natural next step. There is also a regulatory argument: while it is difficult to make the argument that Facebook has broken antitrust laws, the remedy, should that be accomplished, is obvious — split off Instagram and WhatsApp. That will be harder to do if they are fully integrated with Facebook, not simply on the advertising side but also the user side.

Secure Data Storage: This is an interesting addition to this piece, as it has little to do with messaging in the communications sense, but a lot to do with messaging in the political sense. This is what Zuckerberg wrote:

There’s an important difference between providing a service in a country and storing people’s data there. As we build our infrastructure around the world, we’ve chosen not to build data centers in countries that have a track record of violating human rights like privacy or freedom of expression. If we build data centers and store sensitive data in these countries, rather than just caching non-sensitive data, it could make it easier for those governments to take people’s information.

Upholding this principle may mean that our services will get blocked in some countries, or that we won’t be able to enter others anytime soon. That’s a tradeoff we’re willing to make. We do not believe storing people’s data in some countries is a secure enough foundation to build such important internet infrastructure on.

The most obvious country worth avoiding is China, which means this is clearly a Strategy Credit:

A strategy credit is an uncomplicated decision that makes a company look good relative to other companies who face much more significant trade-offs.

Facebook is already banned in China, so not putting data centers in China costs the company nothing (it may soon cost the company in Russia; one imagines Facebook will not mind being banned there of all places). This is in sharp contrast to Facebook’s most vociferous critic in tech, Tim Cook and Apple; the latter absolutely stores customer data in China along with encryption keys, because that is the law for companies that wish to operate in the country.

To be clear, this is understandable, but that is what makes that Strategy Credit article rather ironic; I coined the term in response to Apple’s posturing about user data in the wake of the Snowden revelations, noting that forgoing data wasn’t really a tradeoff given Apple’s business model. Now Apple is on the other side of the coin.

Ultimately there are three broad takeaways from Zuckerberg’s article:

This was a point I made last year in Open, Closed, and Privacy:

If an emphasis on privacy and the non-leakage of data is a priority, it follows that the platforms that already exist will be increasingly entrenched. And, if those platforms will be increasingly entrenched, then the more valuable might regulation be that ensures an equal playing field on top of those platforms. The reality is that an emphasis on privacy will only increase the walls on those gardens; it may be fruitful to rule out the possibility of unfair expansion.

This is a debate that is woefully lacking. The reality is that the only user-friendly way to enforce privacy — which is another way of saying the only scalable way in a demand-driven world — is to severely limit inter-operability and over-burden would-be challengers. Regulators need to be far more aware of this and either choose another approach to privacy — i.e. entrust it to individuals — or regulate data-platforms, at least in terms of competition on top of their platforms, even more severely.

On Exponent, the weekly podcast I host with James Allworth, we discuss The Value Chain Constraint.

Listen to it here.

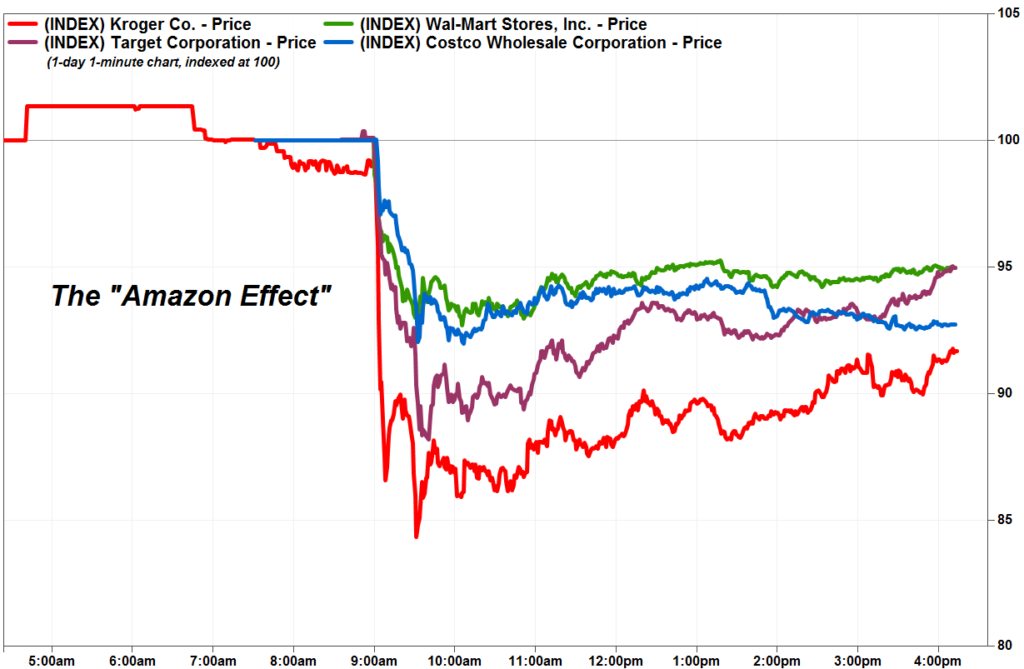

On June 16, 2017, minutes after Amazon announced it was buying Whole Foods Market Inc. for $13.7 billion, grocery store stocks fell through the floor; from MarketWatch (emphasis mine):

Shares of grocery stores took an unexpected hit Friday as investors reeled from the news that Amazon.com Inc. was moving into their space by acquiring Whole Foods Market Inc. After Amazon announced that it was buying Whole Foods in a $13.7 all-cash deal, shares of grocery store chain Kroger Co. slid to close down 9.2%, shares of Costco Wholesale Corp closed down 7.2%, Target Corp.’s stock closed down 5.2% and shares of Wal-Mart Stores Inc. closed down 4.6%…

Mark Hamrick, a senior economic analyst at Bankrate.com, said Amazon’s technological innovation in traditional retail is a “earthquake” for the sector, which it may have hinted at with its recent launches of brick-and-mortar Amazon bookstores. “We can only imagine the technological innovation that Amazon will bring to the purchasing experience for the consumer,” Hamrick said.

This is why I found Walmart’s recent earnings so interesting: the company cited groceries as the biggest drivers of its ecommerce business, both last year and going forward — the company plans to expand grocery pickup to an additional 1,000 stores — because, as Walmart CEO Doug McMillon put it on the company’s earnings call:

We strive to make every day easier for busy families as we increase convenience and save them money and time. Part of our strategy is to build on our existing strengths, such as having a broad assortment including fresh and perishable foods within 10 miles of 90% of the U.S. population.

Amazon, meanwhile, appears to be struggling; from Bloomberg:

The number of Amazon Prime members who shop for groceries at least once a month declined in 2018 compared with 2017, according to the results of an annual consumer survey released Wednesday by UBS analysts. The drop was surprising given the company’s Whole Foods investment and expansion of two hour delivery service Prime Now, the analysts wrote in a note to investors.

A separate study by research firm Brick Meets Click found that households using grocery delivery and pickup services from physical retailers spend about $200 per month and place orders more frequently than Amazon grocery shoppers, who spend $74 a month.

So where is the promised technological innovation?

I have written several times about the Conservation of Attractive Profits, most notably with regards to Netflix, Facebook and BuzzFeed, and Zillow. To put it in generic terms, profit in a value chain flows to whatever company is able to successfully integrate different component pieces of that value chain; the other parts of the value chain then modularize and are driven into commodity competition.

For example, this is what Walmart’s traditional value chain looked like:

Walmart was able to integrate wholesale purchasing with an expansive network of stores; this provided a moat of sustainably lower prices for customer driven by purchasing power over suppliers.

Amazon, though, thanks to technological innovation — specifically, the Internet — was able to build a different integration in the value chain:

Amazon integrated wholesale purchasing and fulfillment centers with Amazon.com, relying on modularized delivery services for distribution; this provided a moat of superior selection and, at least at the beginning, lower prices, and with Prime, superior convenience, at least for non-perishable goods.

Walmart has worked for years to respond to Amazon’s threat; the problem, though, as I explained in 2016’s Walmart and the Multichannel Trap, is that an integration built around stores was fundamentally unsuited to offering the sort of selection and convenience that Amazon does. The company needed to build up an entirely new set of capabilities and integrations, even as Amazon was leveraging theirs to integrate forward into logistics, adding on a 3rd-party marketplace to expand selection even more, and integrating backwards into their own brands. The result is that Amazon has around 50% share in e-commerce while Walmart has less than 5%.

That, though, is precisely why groceries is worth examining: as I explained when Amazon bought Whole Foods, perishable goods are not well-suited to Amazon’s value chain. Superior selection has diminishing returns, quality varies on an item-by-item basis within a single SKU, and, most importantly, the quality of items degrades with time and transport. In other words, they are a great fit for stores, not distribution centers.

In this view, Amazon’s purchase of Whole Foods was an attempt to acquire a first best customer for its grocery delivery operation, one that would efficiently store and sell perishable goods that weren’t suitable for Amazon’s traditional e-commerce model. And, to be clear, this strategy may yet succeed, but only to the extent Amazon builds a completely new set of capabilities and integrations that will probably end up looking a lot like Walmart, which has a massive head start it is clearly taking advantage of.

In other words, what matters is not “technological innovation”; what matters is value chains and the point of integration on which a company’s sustainable differentiation is built; stray too far and even the most fearsome companies become also-rans.

Consider Google, a company that, more than any other, has been predicated on “technological innovation”. This was possible because the company’s core product — Internet search — entered a value chain with no integrations whatsoever. On the supply side there were countless websites and even more individual web pages, increasing exponentially, and on the demand side were a similarly increasing number of Internet users looking for specific content.

Crucially, all of the supply was easily accessible — just link to it — and all of the demand was capturable — they only needed to type in google.com. This meant that the best search engine — and by best, I mean the purest form of the word, i.e. best performing — could win, and so it did. Google was leaps and bounds better than the competition, thanks to its focus on understanding links — the fabric of the web — instead of simply pages, and consumers flocked to it.

This set off the positive cycle I have described in Aggregation Theory: owning demand gave Google increasing power over supply, which came onto Google’s platform on the search engine’s terms, first by optimizing their web pages and later by delivery content directly to Google’s answer boxes, AMP program, etc., all of which increased demand, resulting in a virtuous cycle.

At the same time Google was building out two critical pieces of the value chain in integration with Search: the first was infrastructure — supporting that much demand required huge investments in servers, fiber optic cables, etc. — and the second was advertising. Ultimately the company’s model looked like this:

Note how Google is so dramatically optimized on all three sides of this integration: users, suppliers, and advertisers interact with Google through their own volition, thanks to the infrastructure Google has built to facilitate that interaction, with almost no person-to-person contact with anyone from Google. It is a model that works very, very well — for search and digital advertising, anyways.

Things have not gone so well for Google Cloud. At first glance, selling infrastructure seems like an obvious opportunity for Google, and much ink has been spilled about how the company — any day now! — will threaten Amazon or Microsoft. After all, Google was building out worldwide infrastructure before anyone else, and the company remains at the forefront of technological innovation.

The problem, though, is that the company’s value chain is completely wrong. The world of enterprise software is not a self-serve world (and to the extent it is, AWS dominates the space); what is necessary is an intermediary layer to interact with relatively centralized buyers with completely different expectations from consumers when it comes to product roadmap visibility, customer support, and pricing.

It has taken Google many years to learn this lesson: Google Cloud remains a distant third to AWS and Microsoft with a strategy that simply wasn’t working. I wrote in a November Daily Update upon the occasion of Google Cloud changing CEOs:

A strategy predicated on being “better” on specific product attributes, though, may fit the culture of Google, but it doesn’t necessarily lead to a winning enterprise strategy. To that end, Google Cloud faces three major problems:

- First, Google has not made an effective case about how specifically machine learning can benefit business that is appreciably different than traditional business analytics. That is not to say it can’t, just that the company hasn’t really made the case.

- Second, Google isn’t competing with Lycos and Yahoo: AWS and Microsoft have machine learning offerings of their own, and Microsoft in particular is much more accomplished at productizing offerings in a way that are understandable and approachable to CIOs.

- Third, and most importantly, the technical attributes of a product are only one piece of what matters to success in the enterprise. Just as important are customization, support, and the ability to sell. Google is widely regarded as being the worst in all three areas.